_icon2_300_300.png?v=34562)

-

The gap between cloud ambition and cloud outcomes has never been more costly—or more fixable.

Global cloud spending is projected to cross $905 billion in 2026 and reach $2.9 trillion by 2034. Yet despite nearly two decades of adoption, a landmark 2026 NTT DATA study of more than 2,300 senior decision-makers across 33 countries found that only 14% of organizations have reached the highest level of cloud maturity. The other 86% are leaving value on the table—sometimes at enormous scale.

For enterprise leaders, the question is no longer "Should we invest in cloud?" It is: "How do we actually realize the value of what we've already invested?"

The Value Gap Is Getting Wider, Not Narrower

The numbers are striking. Organizations waste an estimated 27% of their cloud spend every year—roughly $182 billion at gross value, or more than $100 billion even using a conservative definition of actionable waste. More troubling, this rate has held stubbornly between 27–32% every year since 2019, despite years of optimization effort, FinOps adoption, and cost-management tooling.

Enterprises are not failing for lack of effort. They are failing for lack of structure. According to Gartner, most cloud cost overruns stem not from pricing problems but from structural inefficiencies— fragmented ownership, license sprawl, and weak operational enforcement. Licenses are purchased centrally while cloud operations run separately. Cost governance is periodic rather than continuous. The result is familiar: short-term savings followed by long-term cost creep.

Meanwhile, the underlying business stakes keep rising. Worldwide IT spending is expected to reach $6.08 trillion in 2026, driven primarily by cloud and AI infrastructure. The CFO scrutiny that comes with that level of investment is unprecedented. Boards are no longer satisfied with cloud ROI stories that play out over multiple years—CIOs are now expected to demonstrate measurable financial impact within the first 12 months.

The Hidden Cost of Low Maturity

Consider what 86% of organizations are missing when they operate below peak cloud maturity:

-

Enterprises take an average of 31 days to identify and eliminate cloud waste such as idle, orphaned, or unused resources—and 25 days to detect and adjust overprovisioned instances

-

Only 32% of organizations have fully automated cost-saving practices like shutting down idle resources or rightsizing

-

The median cloud efficiency rate has dropped from 80% to 65%—meaning average organizations now run cloud infrastructure at 35% waste

- 54% of cloud waste stems directly from a lack of visibility into costs

The value gap compounds over time. An organization spending $10 million annually on public cloud— not unusual; 33% of enterprises now spend more than $12 million per year—may be forfeiting $2.7 million to $3.5 million every year to structural inefficiency alone.

Why "Cloud-First" Is Not the Same as "Value-First"

The industry spent a decade driving cloud adoption. The mental model that emerged—"move everything to the cloud, savings will follow"—has proven dangerously incomplete.

A critical insight from the 2026 Flexera State of the Cloud Report signals an important maturation: the number of organizations measuring value delivered to business units rose to 64%, up twelve percentage points year over year. At the same time, pure cost-efficiency metrics declined. This is not a retreat from financial discipline—it is an upgrade. It reflects how mature CIOs and CFOs now manage cloud: as a strategic investment, not an IT line item.

Deloitte research on financial services firms identifies a consistent disconnect: organizations whose technology and business stakeholders operate separately consistently underperform on cloud value realization, regardless of the sophistication of their underlying platforms. Cloud value, in other words, is not a technology outcome. It is an organizational one.

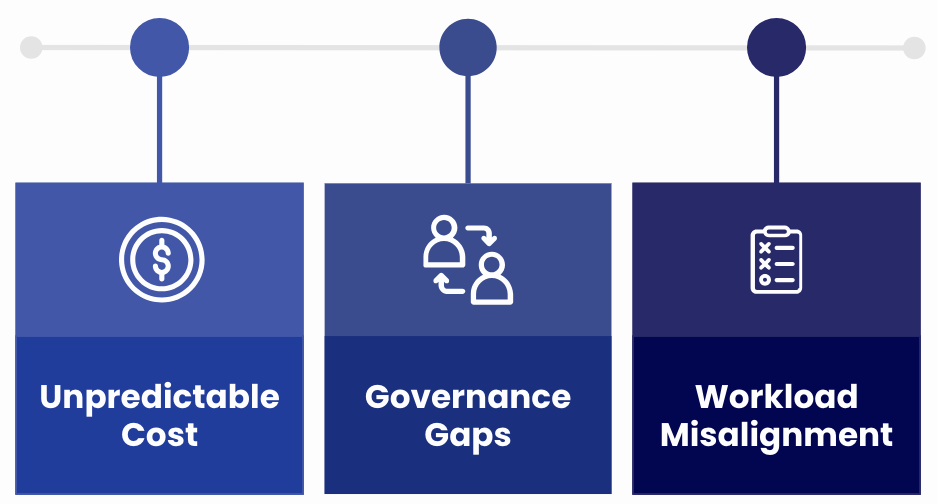

Three Root Causes of Value Leakage

Analysis of enterprise cloud deployments consistently surfaces three interconnected failure modes:

-

Unpredictable Costs — Surprise cloud bills from complex multicloud architectures and insufficient spending visibility. Without proper cost allocation, enterprises cannot connect cloud expenditures to specific business outcomes.

- Governance Gaps — No structured framework to tie cloud spending directly to measurable business outcomes. Cloud investments remain disconnected from strategic objectives. Cost and governance frustration ranks among the top barriers to cloud success.

- Workload Misalignment — Non-optimized workloads maintained in cloud environments without systematic evaluation of whether on-premises or hybrid alternatives offer superior value. A "cloud-first" mentality that persists even when data suggests otherwise.

The Strategic Shift: From Cost Center to Value Engine

The organizations closing the gap share a common posture: they treat cloud not as an infrastructure cost to minimize but as an operational capability to optimize and direct. Forrester's research makes the mandate explicit—CIOs are expected to scale AI and digital initiatives without proportional increases in IT spend. Innovation must increasingly be self-funded.

This creates a virtuous cycle when managed intentionally: disciplined cloud governance reduces structural waste, freeing capital for AI platforms, data modernization, and cloud-native development. The run state funds the change state. The organizations executing this cycle are pulling ahead of those still reacting to quarterly bills.

The 2026 cloud landscape has three defining dynamics:

-

Cloud as AI execution layer — 99% of organizations say AI is increasing demand for cloud investment, yet 88% say current cloud investment levels are putting AI, cloud-native, and modernization initiatives at risk. Cloud and AI strategies must now be developed in tandem, not sequentially.

-

Hybrid and multicloud as the default — 88% of enterprises are operating or deploying hybrid cloud environments, and 79% use multiple cloud providers. Complexity has permanently increased. The governance model must match.

-

Business metrics replacing technical metrics — Cloud success is no longer measured by elasticity or uptime alone. It is measured by faster time-to-market, improved customer experience, higher system reliability, and operational agility.

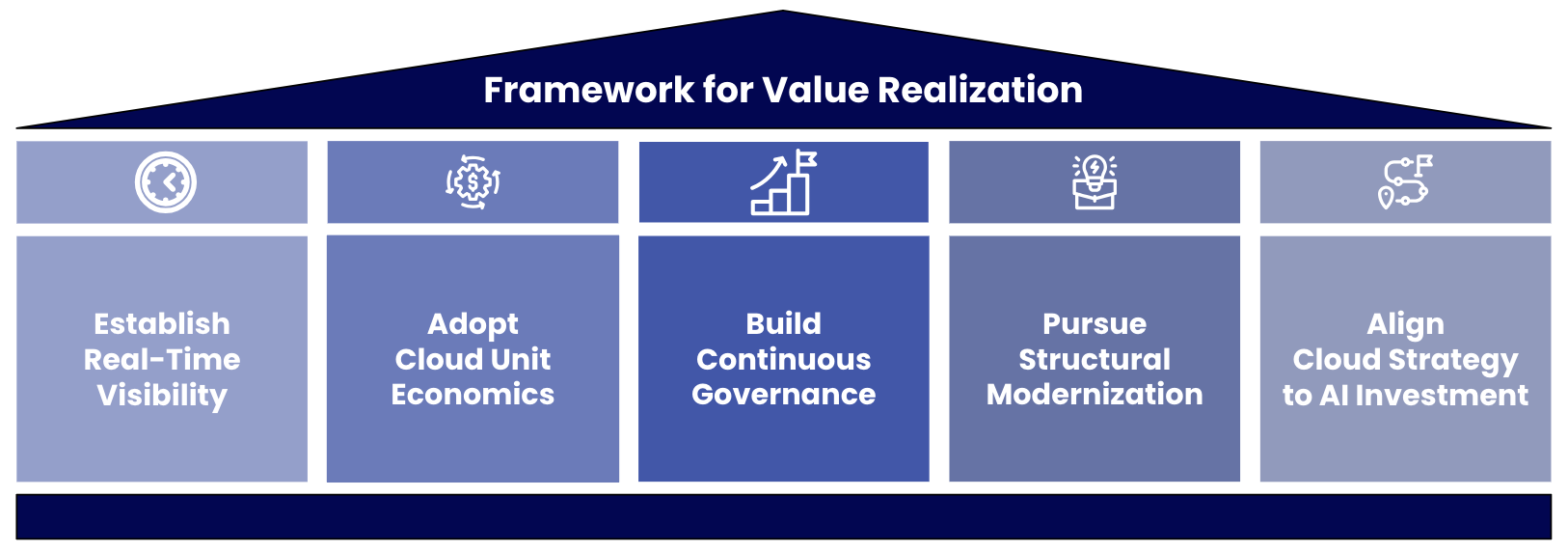

A Framework for Value Realization

Realizing value from cloud investment requires moving beyond one-time optimization events toward a continuously improving operating model. The following five-pillar framework reflects both analyst consensus and leading enterprise practice.

Pillar 1: Establish Real-Time Visibility

You cannot optimize what you cannot see. The foundational step is building real-time visibility into cloud spend—not monthly report reviews but continuous, service-level, workload-level cost mapping. This means:

-

Real-time spend dashboards with anomaly alerts

-

Consistent cost attribution across teams and business units using unified tagging

-

Baseline metrics established before optimization work begins—so improvements can be measured and communicated credibly to the CFO

Organizations that lack this foundation waste 54% of their potential savings simply because they cannot identify where the waste is.

Pillar 2: Adopt Cloud Unit Economics

The most powerful shift in cloud financial management is the move to unit economics: measuring cloud spend per unit of business value produced—cost per customer, cost per transaction, cost per product feature delivered.

Unit economics does three things that traditional cloud cost management cannot:

-

It gives engineering, finance, and business stakeholders a shared language—translating the abstract cloud bill into terms that resonate across the organization.

-

It enables accurate forecasting based on business growth, not just historical infrastructure trends.

-

It reframes rising cloud spend as potentially positive—if cost per unit is declining while total spend is growing, the business is scaling efficiently.

The 2026 Flexera data shows that 49% of organizations now use unit economics to link cloud cost to business outcomes, up from 40% the previous year. The gap between leaders and laggards is increasingly defined by this capability.

Pillar 3: Build Continuous Governance

The most common error in cloud governance is treating it as a periodic event—a quarterly review, an annual optimization sprint. Governance must be embedded into operations continuously.

This means aligning CIO and CFO priorities under a shared accountability model where technology teams retain speed and flexibility while finance teams gain transparency and predictability. Practically, it requires:

-

Ownership assignment: Every cloud resource has an identified owner accountable for its cost and performance

-

Policy enforcement at the architecture level: Governance standards embedded into CI/CD pipelines and deployment workflows, not applied retroactively

-

Continuous license management: Particularly for SaaS and Microsoft estates, where over-licensing of Microsoft 365 E3/E5 licenses remains one of the most persistent sources of enterprise waste

NTT DATA's research shows that organizations at the highest levels of cloud maturity define clear roles and responsibilities backed by regular audits—and are 68% confident in their security posture, versus 36% among less mature peers.

Pillar 4: Pursue Structural Modernization

Enterprises report that legacy applications and data platforms are holding back cloud innovation. Value realization stalls when modern cloud infrastructure runs old application architectures. Modernization is not an optional future phase—it is the mechanism by which cloud investment pays off.

The highest-impact modernization moves:

-

Right-sizing workloads provisioned at 2x–5x actual resource needs(30–50% cost reduction)

-

Containerization: Moving to Kubernetes-based deployments from VMs typically yields 40–60% cost reduction for equivalent workloads

-

Spot and preemptible instances for CI/CD, batch processing, and ML training(60–90% off on-demand rates)

-

Application-level refactoring from monolithic to microservices or serverless architectures where workload patterns support it

A practical lens: for any workload where a modernized architecture delivers more than 30% cost reduction, it belongs on the immediate modernization roadmap.

Pillar 5: Align Cloud Strategy to AI Investment

The arrival of AI as a primary business priority has fundamentally changed the cloud value equation. The AI infrastructure market is projected to grow from $35 billion in 2023 to over $220 billion by 2030 at approximately 30% CAGR. For many organizations, the cloud is now the infrastructure upon which AI runs—which means cloud inefficiency directly constrains AI capability.

NTT DATA's six imperatives for cloud-led AI value make clear that organizations treating cloud and AI as separate strategies will underperform those that develop them in tandem. CAIOs are 22% more likely than CIOs to recognize that AI materially increases cloud investment requirements—a gap that produces misaligned budgets and underbuilt foundations.

Organizations that have closed this gap are seeing real results: 47% of cloud leaders used AI in their last cloud migration project versus 35% of peers. The Kyndryl Readiness Report found 54% of organizations now reporting positive ROI from AI investment—but 61% of leaders say pressure to prove that ROI has intensified over the past year.

The FinOps Maturity Journey

The FinOps Foundation's Crawl-Walk-Run maturity model provides organizations with a structured path from reactive cost management to proactive value creation.

| Stage | Crawl | Walk | Run |

|

Capability Focus |

Visibility into cloud costs and usage; tracking spending; identifying waste |

Cost optimization implementation; forecasting; budget mechanisms; cross-functional collaboration |

Full governance integration with business strategy; unit economics; continuous improvement; automated anomaly detection |

|

Key Outcomes |

Basic cost control; first savings identified |

15–25% cost reduction; shared accountability |

Declining unit costs; cloud as competitive advantage |

Most enterprises currently operate at the Walk level—they have basic optimization practices but have not yet embedded cloud financial management into their strategic operating model. The distance from Walk to Run is primarily an organizational and cultural challenge, not a technical one.

McKinsey's transformation research consistently identifies organizational culture as the dominant barrier to digital transformation success—and organizations that invest heavily in culture change see 5.3x higher success rates than those pursuing technology-only approaches.

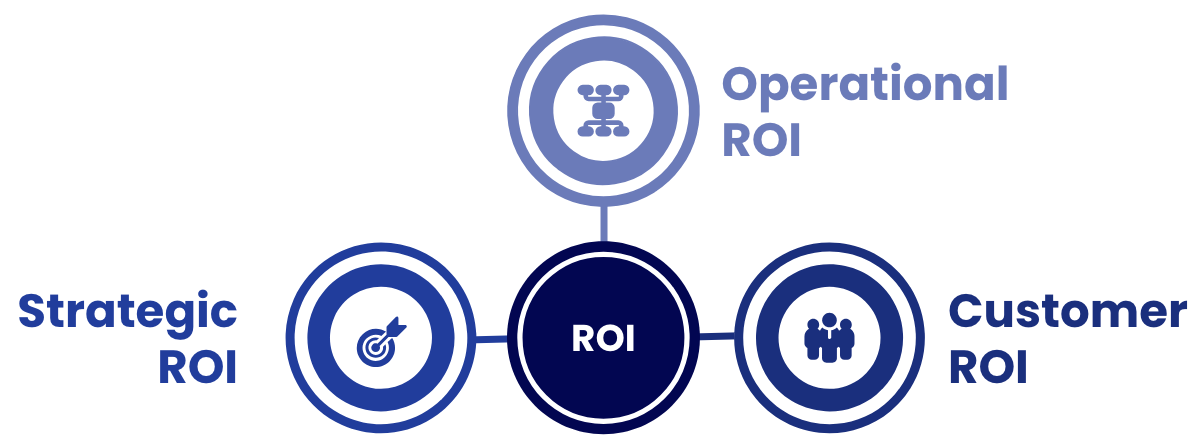

Measuring What Matters: A Business Outcome Scorecard

Effective cloud value realization requires a measurement framework that operates across three dimensions:

Operational ROI

-

Infrastructure cost per workload(before vs. after)

-

Mean time to deploy new services

-

System availability and downtime cost avoidance

Strategic ROI

-

Feature release velocity(time to market)

-

Developer productivity(hours redirected from infrastructure management)

-

Business agility score(ability to respond to market changes)

Customer ROI

-

Customer experience metrics tied to cloud-enabled capabilities

-

Product/service availability and reliability

-

Net Promoter Score changes attributable to digital capability improvements

The 2025 Business Impact Framework establishes that organizations with structured measurement across all three dimensions are significantly better positioned to demonstrate cloud ROI in quarterly earnings discussions. Cloud investments that cannot show up in business performance metrics will face increasing pressure from boards demanding proof of market impact.

What Separates Leaders from Laggards

The 14% of enterprises classified as "cloud evolved" by NTT DATA's 2026 research are significantly better positioned to capitalize on AI and outcompete peers. Their distinguishing behaviors are consistent across industries:

-

They measure business value, not just technical performance — cloud success is defined by customer outcomes and revenue contribution, not uptime SLAs

-

They align cloud and AI investment planning — infrastructure decisions are made in the context of AI roadmaps, not independently

-

They operate continuous governance — ownership, accountability, and cost visibility are embedded in day-to-day operations

-

They modernize deliberately — legacy modernization is a funded, phased strategic program, not a background aspiration

-

They treat cloud efficiency as growth capital — savings from structural optimization are explicitly reinvested into AI, data, and product capabilities

Organizations investing in outcome-based cloud service models—where contracts focus on guaranteed uptime, measurable performance improvements, and specific business outcomes rather than resource consumption—are consistently repositioning cloud from a cost center to a strategic growth enabler.

The Strategic Imperative for 2026 and Beyond

Cloud computing is mature. Cloud value realization is not.

The global cloud market will continue its trajectory toward $5 trillion by 2034. The organizations that capture disproportionate value from that investment will be those that treat cloud as a financial operating discipline, not just a technical infrastructure. They will measure outcomes in business units, govern with continuous rigor, modernize with purpose, and integrate cloud strategy with AI investment from the outset.

For CIOs and CFOs navigating 2026, the message from the data is clear: the next wave of AI and modernization funding will not come from new budget—it will come from how cloud is run today. The organizations that unlock that funding will shape the competitive landscape. Those that do not will keep funding waste instead.

The gap between cloud spend and cloud value is large. It is also addressable. The framework exists, the maturity path is proven, and the business case for getting it right has never been stronger.